生物多样性 ›› 2026, Vol. 34 ›› Issue (4): 25330. DOI: 10.17520/biods.2025330 cstr: 32101.14.biods.2025330

李伯尧1( ), 盛天成2(), 幸小云2,*()(

), 盛天成2(), 幸小云2,*()( )

)

收稿日期:2025-08-18

接受日期:2026-03-17

出版日期:2026-04-20

发布日期:2026-05-27

通讯作者:

*E-mail: xyxing@bjfu.edu.cn

基金资助:

Boyao Li1(), Tiancheng Sheng2(), Xiaoyun Xing2,*()()

Received:2025-08-18

Accepted:2026-03-17

Online:2026-04-20

Published:2026-05-27

Contact:

*E-mail: xyxing@bjfu.edu.cn

Supported by:摘要:

中国作为兼具生态压力与快速发展的新兴经济体, 关于生物多样性风险如何影响企业财务绩效的实证证据仍较为有限。基于2007-2022年中国A股上市公司的面板数据, 本文采用生物多样性风险暴露指数和生物多样性关注指数量化企业层面的风险敞口, 系统检验生物多样性风险对企业资产回报率(ROA)的影响。研究发现, 生物多样性风险显著降低企业财务绩效, 表明生物多样性风险会通过推升合规成本和资源再配置压力侵蚀企业盈利能力。这一负向影响具有显著异质性: 在地理维度上, 市场化程度高、环境规制刚性高的东部地区的风险抑制效应显著强于政策缓冲空间较大的中西部地区; 在所有制维度上, 非国有企业的财务脆弱性显著高于国有企业; 在行业维度上, 生物多样性风险影响和企业应对方式存在明显差异。同时, 绿色产品创新在生物多样性风险与企业财务绩效之间发挥中介作用, 短期内可能因创新投入增加而加重财务压力。本研究在中国情境下为生物多样性风险影响企业基本面提供了微观证据, 并揭示了其在地理、所有制和行业维度上的异质性, 为协调生态文明建设目标与企业可持续发展、完善差异化环境规制和创新激励机制提供了经验依据。

李伯尧, 盛天成, 幸小云 (2026) 生物多样性风险对企业财务绩效的影响: 来自中国上市公司的证据. 生物多样性, 34, 25330. DOI: 10.17520/biods.2025330.

Boyao Li, Tiancheng Sheng, Xiaoyun Xing (2026) Impact of biodiversity risk on corporate financial performance: Evidence from listed companies in China. Biodiversity Science, 34, 25330. DOI: 10.17520/biods.2025330.

| 变量类型 | 变量名称 | 英文全称 | 变量符号 | 变量度量 |

| 被解释变量 | 资产回报率 | Return on assets | ROA | 净利润/总资产 |

| 解释变量 | 生物多样性风险暴露指数 | Biodiversity Exposure Index | BE | 由关键词词频赋值 |

| 生物多样性关注指数 | Biodiversity Concern Index | BC | 关键词词频占比 | |

| 控制变量 | 企业规模 | Firm size | Size | 总资产取对数 |

| 资产负债率 | Leverage ratio | Lev | 总负债/总资产 | |

| 营收增长率 | Revenue growth rate | Growth | 本年营业收入总额/上一年营业收入总额 |

Box 1 变量详细信息

| 变量类型 | 变量名称 | 英文全称 | 变量符号 | 变量度量 |

| 被解释变量 | 资产回报率 | Return on assets | ROA | 净利润/总资产 |

| 解释变量 | 生物多样性风险暴露指数 | Biodiversity Exposure Index | BE | 由关键词词频赋值 |

| 生物多样性关注指数 | Biodiversity Concern Index | BC | 关键词词频占比 | |

| 控制变量 | 企业规模 | Firm size | Size | 总资产取对数 |

| 资产负债率 | Leverage ratio | Lev | 总负债/总资产 | |

| 营收增长率 | Revenue growth rate | Growth | 本年营业收入总额/上一年营业收入总额 |

| 变量 Variables | 观测值 Observations | 平均值 Mean | 标准差 Standard deviation | 最小值 Minimum | 最大值 Maximum |

|---|---|---|---|---|---|

| ROA | 40,932 | 0.041 | 0.061 | -0.223 | 0.208 |

| BE | 40,932 | 0.436 | 0.496 | 0.000 | 1.000 |

| BC | 40,932 | 0.000 | 0.000 | 0.000 | 0.010 |

| Size | 40,931 | 22.115 | 1.333 | 14.158 | 28.636 |

| Lev | 40,932 | 0.417 | 0.205 | 0.051 | 0.888 |

| Growth | 40,901 | 0.171 | 0.372 | -0.527 | 2.213 |

表1 主要财务与生物多样性风险相关变量的描述性统计

Table 1 Descriptive statistics of the main financial and biodiversity risk-related variables

| 变量 Variables | 观测值 Observations | 平均值 Mean | 标准差 Standard deviation | 最小值 Minimum | 最大值 Maximum |

|---|---|---|---|---|---|

| ROA | 40,932 | 0.041 | 0.061 | -0.223 | 0.208 |

| BE | 40,932 | 0.436 | 0.496 | 0.000 | 1.000 |

| BC | 40,932 | 0.000 | 0.000 | 0.000 | 0.010 |

| Size | 40,931 | 22.115 | 1.333 | 14.158 | 28.636 |

| Lev | 40,932 | 0.417 | 0.205 | 0.051 | 0.888 |

| Growth | 40,901 | 0.171 | 0.372 | -0.527 | 2.213 |

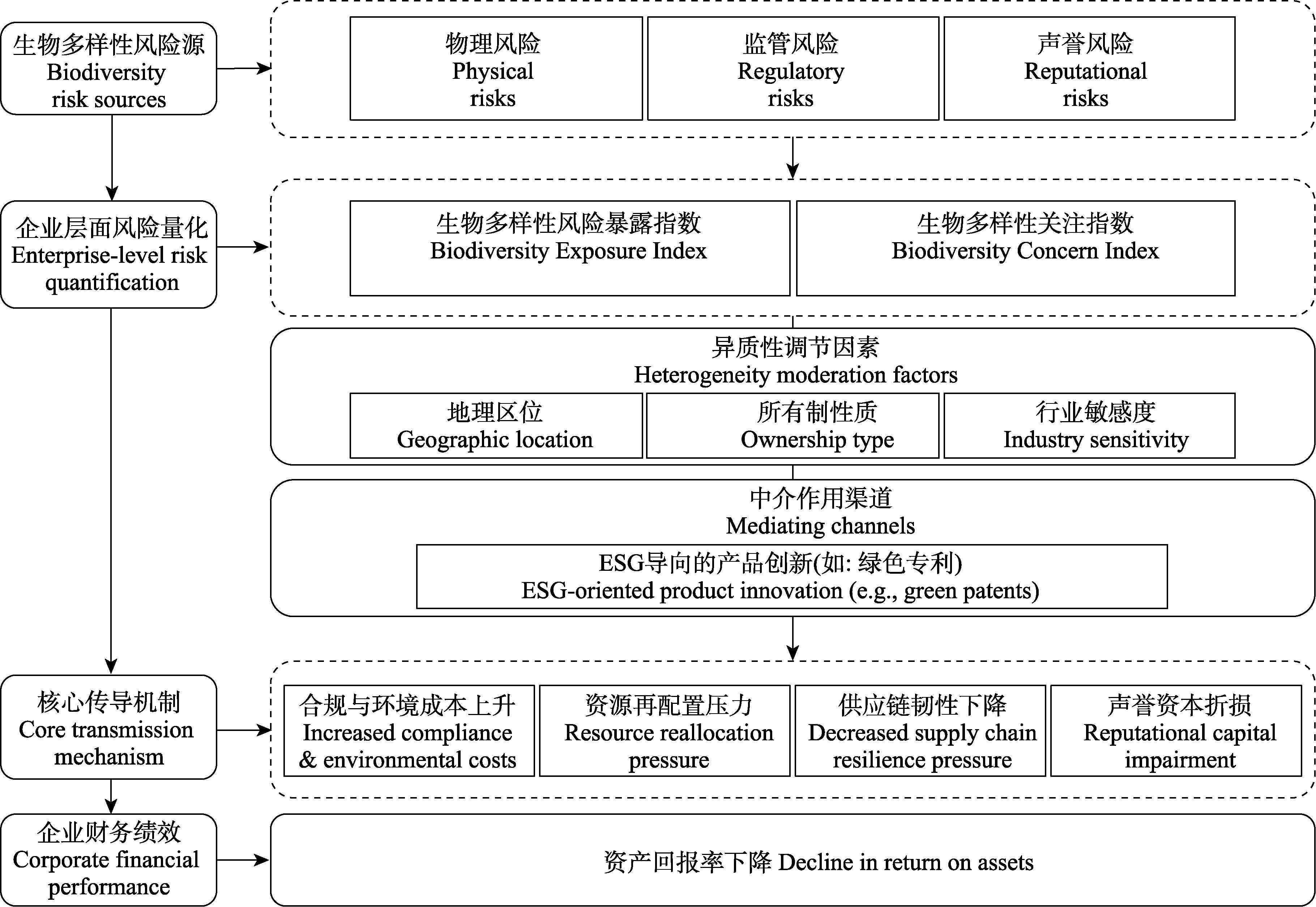

图1 生物多样性风险与企业财务绩效关系的概念框架。ESG: 环境、社会与治理。

Fig. 1 Conceptual framework of the relationship between biodiversity risk and corporate financial performance. ESG, Environmental, social and governance.

| 变量 Variables | BE模型 BE model | BC模型 BC model |

|---|---|---|

| 被解释变量 DV | ROA | ROA |

| BE | -0.002345*** | |

| (0.000605) | ||

| BC | -2.018842*** | |

| (0.656294) | ||

| Size | 0.009733*** | 0.009573*** |

| (0.000279) | (0.000274) | |

| Lev | -0.147774*** | -0.147735*** |

| (0.001890) | (0.001890) | |

| Growth | 0.040498*** | 0.040458*** |

| (0.001009) | (0.001009) | |

| 常数项 Constant | -0.118338*** | -0.115637*** |

| (0.005741) | (0.005676) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes |

| 观测值 Observations | 40,900 | 40,900 |

| 调整后R2 Adjusted R2 | 0.252565 | 0.252408 |

表2 生物多样性风险对企业财务绩效影响的基准回归结果

Table 2 Benchmark regression results of the impact of biodiversity risk on corporate financial performance

| 变量 Variables | BE模型 BE model | BC模型 BC model |

|---|---|---|

| 被解释变量 DV | ROA | ROA |

| BE | -0.002345*** | |

| (0.000605) | ||

| BC | -2.018842*** | |

| (0.656294) | ||

| Size | 0.009733*** | 0.009573*** |

| (0.000279) | (0.000274) | |

| Lev | -0.147774*** | -0.147735*** |

| (0.001890) | (0.001890) | |

| Growth | 0.040498*** | 0.040458*** |

| (0.001009) | (0.001009) | |

| 常数项 Constant | -0.118338*** | -0.115637*** |

| (0.005741) | (0.005676) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes |

| 观测值 Observations | 40,900 | 40,900 |

| 调整后R2 Adjusted R2 | 0.252565 | 0.252408 |

| 变量 Variables | L.BE模型 L.BE model | L.BC模型 L.BC model |

|---|---|---|

| 被解释变量 DV | ROA | ROA |

| L.BE | -0.003159*** | |

| (0.000642) | ||

| L.BC | -2.809240*** | |

| (0.736606) | ||

| 常数项 Constant | -0.172160*** | -0.168500*** |

| (0.005774) | (0.005709) | |

| 控制变量 Control variables | 是 Yes | 是 Yes |

| 固定效应 Fixed effects | 是 Yes | 是 Yes |

| 观测值 Observations | 35,893 | 35,893 |

| 调整后R2 Adjusted R2 | 0.263539 | 0.263256 |

表3 生物多样性风险对企业财务绩效影响的滞后效应模型回归结果

Table 3 Regression results of the lag effect model for the impact of biodiversity risk on corporate financial performance

| 变量 Variables | L.BE模型 L.BE model | L.BC模型 L.BC model |

|---|---|---|

| 被解释变量 DV | ROA | ROA |

| L.BE | -0.003159*** | |

| (0.000642) | ||

| L.BC | -2.809240*** | |

| (0.736606) | ||

| 常数项 Constant | -0.172160*** | -0.168500*** |

| (0.005774) | (0.005709) | |

| 控制变量 Control variables | 是 Yes | 是 Yes |

| 固定效应 Fixed effects | 是 Yes | 是 Yes |

| 观测值 Observations | 35,893 | 35,893 |

| 调整后R2 Adjusted R2 | 0.263539 | 0.263256 |

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||

|---|---|---|---|---|

| 第一阶段 First stage | 第二阶段 Second stage | 第一阶段 First stage | 第二阶段 Second stage | |

| 被解释变量 DV | BE | ROA | BC1e6 | ROA |

| IV_BE | 0.674891*** | |||

| (0.059) | ||||

| BE | -0.031078*** | |||

| (0.010) | ||||

| IV_BC1e6 | 0.231670*** | |||

| (0.053) | ||||

| BC1e6 | -0.000058* | |||

| (0.000) | ||||

| Size | 0.081096 | 0.013647 | 11.520616*** | 0.011495*** |

| (0.003) | (0.000905) | (0.907) | (0.000) | |

| Lev | -0.036283 | -0.158496 | -5.530266 | -0.155529*** |

| (0.016) | (0.002) | (5.902) | (0.002) | |

| Growth | -0.005389 | 0.048850 | -8.561463*** | 0.053751*** |

| (0.008) | (0.001) | (3.108) | (0.001) | |

| 常数项 Constant | -1.578773*** | -0.173306*** | 9.835776 | -0.124574*** |

| (0.071) | (0.015) | (25.193) | (0.008) | |

| F统计量 Cragg-Donald Wald F | 128.92 | 107.557 | ||

| Anderson-Rubin 95%置信区间 Anderson-Rubin 95% confidence interval | [-0.051566, -0.010590] | [-.0001114, -4.49e-06] | ||

| 观测值 Observations | 26,209 | 26,209 | 26,209 | 26,209 |

| R2 | 0.262 | 0.239 | 0.158 | 0.277 |

| 调整后R2 Adjusted R2 | 0.261 | 0.157 | ||

表4 行业同群工具变量法回归结果

Table 4 Regression results using the industry peer instrumental variable method

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||

|---|---|---|---|---|

| 第一阶段 First stage | 第二阶段 Second stage | 第一阶段 First stage | 第二阶段 Second stage | |

| 被解释变量 DV | BE | ROA | BC1e6 | ROA |

| IV_BE | 0.674891*** | |||

| (0.059) | ||||

| BE | -0.031078*** | |||

| (0.010) | ||||

| IV_BC1e6 | 0.231670*** | |||

| (0.053) | ||||

| BC1e6 | -0.000058* | |||

| (0.000) | ||||

| Size | 0.081096 | 0.013647 | 11.520616*** | 0.011495*** |

| (0.003) | (0.000905) | (0.907) | (0.000) | |

| Lev | -0.036283 | -0.158496 | -5.530266 | -0.155529*** |

| (0.016) | (0.002) | (5.902) | (0.002) | |

| Growth | -0.005389 | 0.048850 | -8.561463*** | 0.053751*** |

| (0.008) | (0.001) | (3.108) | (0.001) | |

| 常数项 Constant | -1.578773*** | -0.173306*** | 9.835776 | -0.124574*** |

| (0.071) | (0.015) | (25.193) | (0.008) | |

| F统计量 Cragg-Donald Wald F | 128.92 | 107.557 | ||

| Anderson-Rubin 95%置信区间 Anderson-Rubin 95% confidence interval | [-0.051566, -0.010590] | [-.0001114, -4.49e-06] | ||

| 观测值 Observations | 26,209 | 26,209 | 26,209 | 26,209 |

| R2 | 0.262 | 0.239 | 0.158 | 0.277 |

| 调整后R2 Adjusted R2 | 0.261 | 0.157 | ||

| 变量 Variables | BE模型 BE model | BC模型 BC model | 多期滞后模型 Multi-period lag model |

|---|---|---|---|

| 被解释变量 DV | ROE | ROE | ROA |

| BE | -0.003389** | ||

| (0.001347) | |||

| BC | -6.314404*** | ||

| (1.884943) | |||

| L.BE | -0.001457 | ||

| (0.001270) | |||

| L2.BE | -0.001346 | ||

| (0.001397) | |||

| L3.BE | -0.002074 | ||

| (0.001312) | |||

| L.BC | 5.742202* | ||

| (3.108998) | |||

| L2.BC | -1.060511 | ||

| (4.739165) | |||

| L3.BC | -6.349210* | ||

| (3.827503) | |||

| 常数项 Constant | -0.374697*** | -0.371332*** | -0.225105*** |

| (0.014080) | (0.013942) | (0.009404) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 40,835 | 40,835 | 13,697 |

| 调整后R2 Adjusted R2 | 0.162266 | 0.162400 | 0.2869 |

表5 稳健性检验和多期滞后模型回归结果

Table 5 Robustness test and multi-period lag model regression results

| 变量 Variables | BE模型 BE model | BC模型 BC model | 多期滞后模型 Multi-period lag model |

|---|---|---|---|

| 被解释变量 DV | ROE | ROE | ROA |

| BE | -0.003389** | ||

| (0.001347) | |||

| BC | -6.314404*** | ||

| (1.884943) | |||

| L.BE | -0.001457 | ||

| (0.001270) | |||

| L2.BE | -0.001346 | ||

| (0.001397) | |||

| L3.BE | -0.002074 | ||

| (0.001312) | |||

| L.BC | 5.742202* | ||

| (3.108998) | |||

| L2.BC | -1.060511 | ||

| (4.739165) | |||

| L3.BC | -6.349210* | ||

| (3.827503) | |||

| 常数项 Constant | -0.374697*** | -0.371332*** | -0.225105*** |

| (0.014080) | (0.013942) | (0.009404) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 40,835 | 40,835 | 13,697 |

| 调整后R2 Adjusted R2 | 0.162266 | 0.162400 | 0.2869 |

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||||

|---|---|---|---|---|---|---|

| 西部地区 Western region | 东部地区 Eastern region | 中部地区 Central region | 西部地区 Western region | 东部地区 Eastern region | 中部地区 Central region | |

| 被解释变量 DV | ROA | ROA | ROA | ROA | ROA | ROA |

| BE | 0.001751 | -0.003500*** | 0.000243 | |||

| (0.001812) | (0.000726) | (0.001569) | ||||

| BC | -0.456884 | -1.875953** | -6.000618*** | |||

| (1.710981) | (0.763839) | (2.211839) | ||||

| 常数项 Constant | -0.187840*** | -0.108552*** | -0.183010*** | -0.189985*** | -0.104058*** | -0.183394*** |

| (0.016963) | (0.006692) | (0.015754) | (0.016909) | (0.006603) | (0.015674) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 4,965 | 27,735 | 6,193 | 4,965 | 27,735 | 6,193 |

| 调整后R2 Adjusted R2 | 0.304304 | 0.244027 | 0.288845 | 0.304172 | 0.243508 | 0.289331 |

表6 不同地理区域的异质性回归结果

Table 6 Heterogeneity analysis of different geographical regions

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||||

|---|---|---|---|---|---|---|

| 西部地区 Western region | 东部地区 Eastern region | 中部地区 Central region | 西部地区 Western region | 东部地区 Eastern region | 中部地区 Central region | |

| 被解释变量 DV | ROA | ROA | ROA | ROA | ROA | ROA |

| BE | 0.001751 | -0.003500*** | 0.000243 | |||

| (0.001812) | (0.000726) | (0.001569) | ||||

| BC | -0.456884 | -1.875953** | -6.000618*** | |||

| (1.710981) | (0.763839) | (2.211839) | ||||

| 常数项 Constant | -0.187840*** | -0.108552*** | -0.183010*** | -0.189985*** | -0.104058*** | -0.183394*** |

| (0.016963) | (0.006692) | (0.015754) | (0.016909) | (0.006603) | (0.015674) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 4,965 | 27,735 | 6,193 | 4,965 | 27,735 | 6,193 |

| 调整后R2 Adjusted R2 | 0.304304 | 0.244027 | 0.288845 | 0.304172 | 0.243508 | 0.289331 |

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||

|---|---|---|---|---|

| 国有企业 State-owned corporate | 非国有企业 Non-state-owned corporate | 国有企业 State-owned corporate | 非国有企业 Non-state-owned corporate | |

| 被解释变量 DV | ROA | ROA | ROA | ROA |

| BE | 0.000579 | -0.003282*** | ||

| (0.000929) | (0.000810) | |||

| BC | -0.645367 | -2.461043*** | ||

| (1.208398) | (0.791905) | |||

| 常数项 Constant | -0.138379*** | -0.145665*** | -0.139078*** | -0.141431*** |

| (0.007746) | (0.009137) | (0.007694) | (0.009026) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 14,268 | 24,075 | 14,268 | 24,075 |

| 调整后R2 Adjusted R2 | 0.280578 | 0.242326 | 0.280571 | 0.241996 |

表7 不同所有制性质的回归结果

Table 7 Heterogeneity analysis by ownership type

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||

|---|---|---|---|---|

| 国有企业 State-owned corporate | 非国有企业 Non-state-owned corporate | 国有企业 State-owned corporate | 非国有企业 Non-state-owned corporate | |

| 被解释变量 DV | ROA | ROA | ROA | ROA |

| BE | 0.000579 | -0.003282*** | ||

| (0.000929) | (0.000810) | |||

| BC | -0.645367 | -2.461043*** | ||

| (1.208398) | (0.791905) | |||

| 常数项 Constant | -0.138379*** | -0.145665*** | -0.139078*** | -0.141431*** |

| (0.007746) | (0.009137) | (0.007694) | (0.009026) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 14,268 | 24,075 | 14,268 | 24,075 |

| 调整后R2 Adjusted R2 | 0.280578 | 0.242326 | 0.280571 | 0.241996 |

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||||

|---|---|---|---|---|---|---|

| 高敏感度行业 High-sensitivity industry | 中敏感度行业 Medium-sensitivity industry | 低敏感度行业 Low-sensitivity industry | 高敏感度行业 High-sensitivity industry | 中敏感度行业 Medium-sensitivity industry | 低敏感度行业 Low-sensitivity industry | |

| 被解释变量 DV | ROA | ROA | ROA | ROA | ROA | ROA |

| BE | 0.0070411* | 0.0035652*** | -0.001037 | |||

| (0.0029809) | (0.0007842) | (0.0027549) | ||||

| BC | -2.773192* | 1.617218* | -12.92617 | |||

| (1.329168) | (0.6517192) | (13.16067) | ||||

| 常数项 Constant | 0.0594131*** | 0.0855468*** | 0.0660308*** | 0.0656899*** | 0.0866187*** | 0.0664181*** |

| (0.0052501) | (0.0008765) | (0.0024934) | (0.0048338) | (0.0008458) | (0.002416) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 1,409 | 21,856 | 2,538 | 1,409 | 21,856 | 2,538 |

| R2 | 0.2298 | 0.2526 | 0.2065 | 0.2287 | 0.2520 | 0.2069 |

| 调整后R2 Adjusted R2 | 0.2187 | 0.2519 | 0.1996 | 0.2176 | 0.2512 | 0.2000 |

表8 生物多样性风险暴露指数(BE)和生物多样性关注指数(BC)与行业敏感性的回归结果

Table 8 Regression results of Biodiversity Exposure Index (BE) and Biodiversity Concern Index (BC) with industry sensitivity

| 变量 Variables | BE模型 BE model | BC模型 BC model | ||||

|---|---|---|---|---|---|---|

| 高敏感度行业 High-sensitivity industry | 中敏感度行业 Medium-sensitivity industry | 低敏感度行业 Low-sensitivity industry | 高敏感度行业 High-sensitivity industry | 中敏感度行业 Medium-sensitivity industry | 低敏感度行业 Low-sensitivity industry | |

| 被解释变量 DV | ROA | ROA | ROA | ROA | ROA | ROA |

| BE | 0.0070411* | 0.0035652*** | -0.001037 | |||

| (0.0029809) | (0.0007842) | (0.0027549) | ||||

| BC | -2.773192* | 1.617218* | -12.92617 | |||

| (1.329168) | (0.6517192) | (13.16067) | ||||

| 常数项 Constant | 0.0594131*** | 0.0855468*** | 0.0660308*** | 0.0656899*** | 0.0866187*** | 0.0664181*** |

| (0.0052501) | (0.0008765) | (0.0024934) | (0.0048338) | (0.0008458) | (0.002416) | |

| 固定效应 Fixed effects | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes | 是 Yes |

| 观测值 Observations | 1,409 | 21,856 | 2,538 | 1,409 | 21,856 | 2,538 |

| R2 | 0.2298 | 0.2526 | 0.2065 | 0.2287 | 0.2520 | 0.2069 |

| 调整后R2 Adjusted R2 | 0.2187 | 0.2519 | 0.1996 | 0.2176 | 0.2512 | 0.2000 |

| 效应路径 Effect path | BE模型 BE model | BC模型 BC model | ||||||

|---|---|---|---|---|---|---|---|---|

| 系数 Coefficient | 标准误 SE | 95%置信区 间下限 95% CIL | 95%置信区 间上限 95% CIU | 系数 Coefficient | 标准误 SE | 95%置信区 间下限 95% CIL | 95%置信区 间上限 95% CIU | |

| 间接效应 Indirect effects | -2.71×10-5 | 1.18×10-5 | -5.21×10-5 | -5.57×10-6 | -7.21×10-2 | 2.83×10-2 | -1.43×10-1 | -2.72×10-2 |

| 直接效应 Direct effects | -2.02×10-3 | 6.02×10-4 | -3.23×10-3 | -9.11×10-4 | -1.78 | 6.60×10-1 | -3.15 | -5.02×10-1 |

| 自变项→中介项 Independent variable → mediator | 4.19×10-2 | 1.71×10-2 | 7.22×10-3 | 7.47×10-2 | 1.12×102 | 3.89×101 | 4.29×101 | 1.96×102 |

| 中介项→因变项 Mediator→dependent variable | -6.48×10-4 | 1.22×10-4 | -8.96×10-4 | -4.16×10-4 | -6.46×10-4 | 1.22×10-4 | -8.98×10-4 | -4.15×10-4 |

| 总效应 Total effects | -2.35×10-3 | 6.02×10-4 | -3.57×10-3 | -1.25×10-3 | -2.02 | 6.69×10-1 | -3.46 | -7.38×10-1 |

表9 生物多样性风险暴露与生物多样性关注分别通过绿色创新影响财务绩效的中介效应Bootstrap检验结果

Table 9 Bootstrap test results of the mediation effects of biodiversity risk exposure and biodiversity concern on financial performance respectively through green innovation

| 效应路径 Effect path | BE模型 BE model | BC模型 BC model | ||||||

|---|---|---|---|---|---|---|---|---|

| 系数 Coefficient | 标准误 SE | 95%置信区 间下限 95% CIL | 95%置信区 间上限 95% CIU | 系数 Coefficient | 标准误 SE | 95%置信区 间下限 95% CIL | 95%置信区 间上限 95% CIU | |

| 间接效应 Indirect effects | -2.71×10-5 | 1.18×10-5 | -5.21×10-5 | -5.57×10-6 | -7.21×10-2 | 2.83×10-2 | -1.43×10-1 | -2.72×10-2 |

| 直接效应 Direct effects | -2.02×10-3 | 6.02×10-4 | -3.23×10-3 | -9.11×10-4 | -1.78 | 6.60×10-1 | -3.15 | -5.02×10-1 |

| 自变项→中介项 Independent variable → mediator | 4.19×10-2 | 1.71×10-2 | 7.22×10-3 | 7.47×10-2 | 1.12×102 | 3.89×101 | 4.29×101 | 1.96×102 |

| 中介项→因变项 Mediator→dependent variable | -6.48×10-4 | 1.22×10-4 | -8.96×10-4 | -4.16×10-4 | -6.46×10-4 | 1.22×10-4 | -8.98×10-4 | -4.15×10-4 |

| 总效应 Total effects | -2.35×10-3 | 6.02×10-4 | -3.57×10-3 | -1.25×10-3 | -2.02 | 6.69×10-1 | -3.46 | -7.38×10-1 |

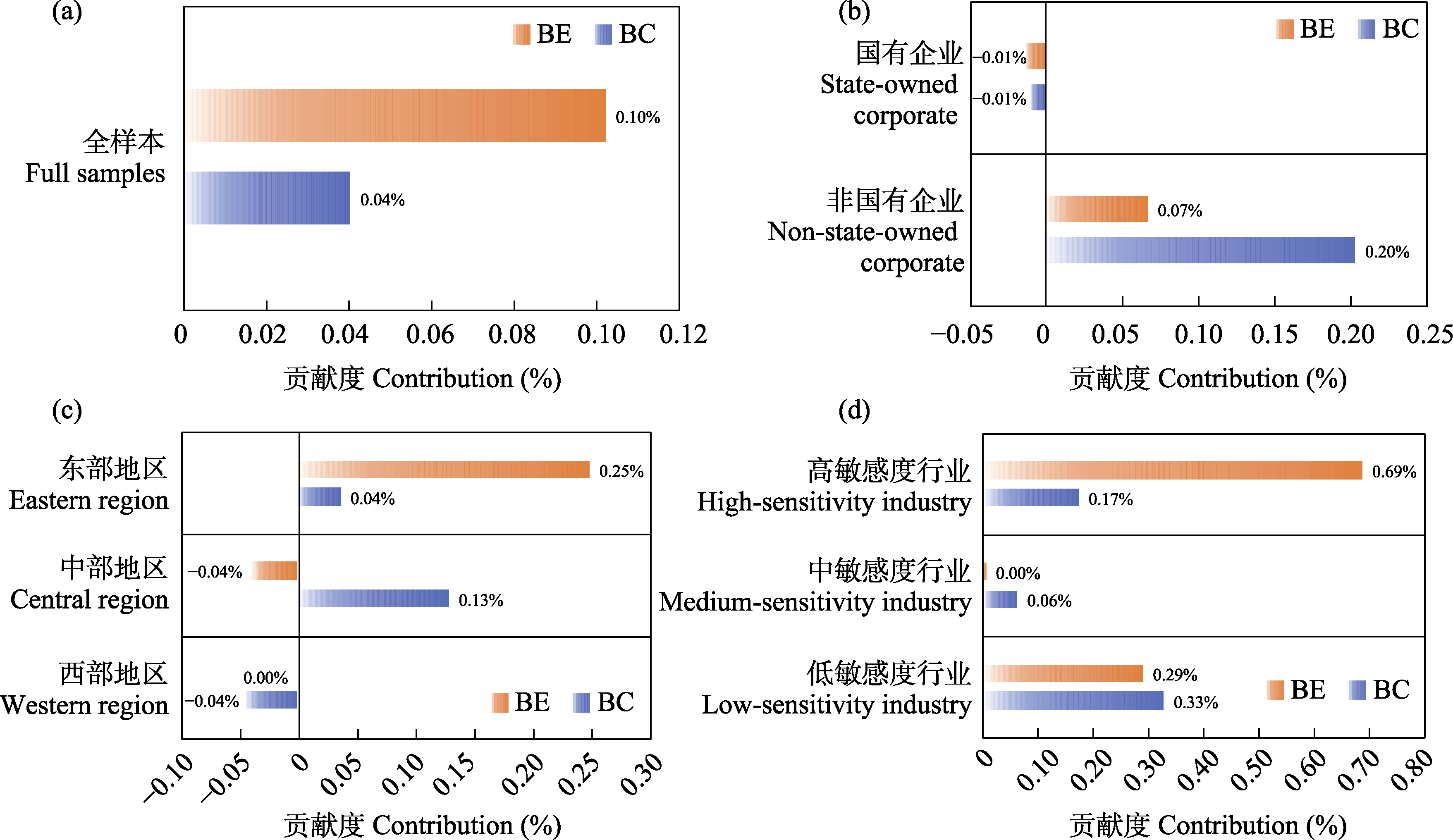

图2 生物多样性风险对企业财务绩效影响的贡献度。BE: 生物多样性风险暴露指数; BC: 生物多样性关注指数。

Fig. 2 Contribution of biodiversity risk to corporate financial performance. BE, Biodiversity Exposure Index; BC, Biodiversity Concern Index.

| [1] |

An H, Chen CR, Wu Q, Zhang T (2021) Corporate innovation: Do diverse boards help? Journal of Financial and Quantitative Analysis, 56, 155-182.

DOI URL |

| [2] | Bach TN, Hoang K, Le T (2025) Biodiversity risk and firm performance: Evidence from US firms. Business Strategy and the Environment, 34, 1113-1132. |

| [3] |

Barney J (1991) Firm resources and sustained competitive advantage. Journal of Management, 17, 99-120.

DOI URL |

| [4] |

Bastien-Olvera BA, Moore FC (2021) Use and non-use value of nature and the social cost of carbon. Nature Sustainability, 4, 101-108.

DOI |

| [5] | Chen ZHJ, Derwall J, Gao X, Koedijk K (2025) Does Biodiversity Risk Matter to Capital Markets? New Evidence from China. https://cepr.org/publications/dp20066. (accessed on 2025-03-19) |

| [6] |

Cosma S, Cosma S, Pennetta D, Rimo G (2025) Does biodiversity matter for firm value? Journal of International Financial Markets, Institutions and Money, 105, 102240.

DOI URL |

| [7] |

Cui CY, Hou YL, Wang TY, Wen YL (2022) Biodiversity conservation supported by finance: Global practice and policy enlightenment. Biodiversity Science, 30, 22326.(in Chinese with English abstract)

DOI |

|

[崔楚云, 侯一蕾, 王天一, 温亚利 (2022) 金融支持生物多样性保护: 全球实践及政策启示. 生物多样性, 30, 22326.]

DOI |

|

| [8] |

Elsayed RAA (2023) Exploring the financial consequences of biodiversity disclosure: How does biodiversity disclosure affect firms’ financial performance? Future Business Journal, 9, 22.

DOI |

| [9] | Fang XM, Hu D (2023) Corporate ESG performance and innovation: Empirical evidence from A-share listed companies. Economic Research Journal, 58(2), 91-106.(in Chinese) |

| [方先明, 胡丁 (2023) 企业ESG表现与创新——来自A股上市公司的证据. 经济研究, 58(2), 91-106.] | |

| [10] | Giglio S, Kuchler T, Stroebel J, Zeng XR (2023) Biodiversity risk. https://doi.org/10.3386/w31137. (accessed on 2025-04-17) |

| [11] |

Hart SL (1995) A natural-resource-based view of the firm. The Academy of Management Review, 20, 986.

DOI URL |

| [12] |

He F, Chen LX, Lucey BM (2024) Chinese corporate biodiversity exposure. Finance Research Letters, 70, 106275.

DOI URL |

| [13] |

Houdet J, Trommetter M, Weber J (2012) Understanding changes in business strategies regarding biodiversity and ecosystem services. Ecological Economics, 73, 37-46.

DOI URL |

| [14] | IPBES (Intergovernmental Science-Policy Platform for Biodiversity and Ecosystem Services) (2019) Global Assessment Report on Biodiversity and Ecosystem Services. https://zenodo.org/records/3553579. (accessed on 2024-11-25) |

| [15] | Johnson JA, Baldos U, Cervigni R, Chonabayashi S, Corong E, Gavryliuk O, Hertel T, Nootenboom C, Gerber J, Ruta G, Polasky S (2021) The Economic Case for Nature: A Global Earth-Economy Model to Assess Development Policy Pathways. https://hdl.handle.net/10986/35882. (accessed on 2025-06-29) |

| [16] |

Kong DM, Zhang BH, Zhang J (2022) Higher education and corporate innovation. Journal of Corporate Finance, 72, 102165.

DOI URL |

| [17] | Li XQ, Dong ZF, Ge CZ, Li XL (2022) Study on innovative policy for financing biodiversity. Environmental Protection, 50(8), 28-31.(in Chinese with English abstract) |

| [李晓琼, 董战峰, 葛察忠, 李晓亮 (2022) 生物多样性保护的金融政策创新研究. 环境保护, 50(8), 28-31.] | |

| [18] | Liu Z, Kong LQ, Zhang JB (2025) Green finance and biodiversity: Empirical research based on Chinese bird watching data. China Economic Quarterly, 25, 565-580.(in Chinese with English abstract) |

| [刘钊, 孔令乾, 张俊飚 (2025) 绿色金融与生物多样性——基于中国观鸟数据的考察. 经济学(季刊), 25, 565-580.] | |

| [19] | National Bureau of Statistics (2017) Industrial Classification for National Economic Activities.(in Chinese) |

| [国家统计局 (2017) 国民经济行业分类.] https://www.stats.gov.cn/xxgk/tjbz/gjtjbz/202008/P020200811606493723477.pdf. (accessed on 2025-05-31) | |

| [20] | North DC (1990) Institutions, Institutional Change and Economic Performance. Cambridge University Press, Cambridge, UK. |

| [21] | Qiao Q, Yu QR, Feng L, Chen L, Liu CL, Li A (2024) Establishment of an indicator system for assessing corporate biodiversity performance. Research of Environmental Sciences, 37, 2324-2332.(in Chinese with English abstract) |

| [乔青, 于倩茹, 冯乐, 陈龙, 刘春兰, 李昂 (2024) 企业生物多样性绩效评估指标体系构建. 环境科学研究, 37, 2324-2332.] | |

| [22] | Rao A, Lucey BM, Kumar S (2024) Corporate Biodiversity Risk and Concern: Evidence from Indian Firms and Industry-level Insights. https://papers.ssrn.com/sol3/Delivery.cfm?abstractid=4986392. (accessed on 2024-12-03) |

| [23] | Stiglitz JE, Weiss A (1981) Credit rationing in markets with imperfect information. The American Economic Review, 71, 393-410. |

| [24] |

Tang XM, Qin T (2025) Chinese enterprises’ biodiversity disclosure index construction and financing effects. Biodiversity Science, 33, 24264.(in Chinese with English abstract)

DOI |

|

[汤心萌, 秦涛 (2025) 中国企业生物多样性信息披露指数构建及融资效应. 生物多样性, 33, 24264.]

DOI |

|

| [25] | Tao YN, Yuan J (2022) Impact and enlightenment of biodiversity decline on industrial chain security and financial stability. South China Finance, (2), 72-78.(in Chinese with English abstract) |

| [陶娅娜, 袁佳 (2022) 生物多样性下降对产业链安全及金融稳定的影响与启示. 南方金融, (2), 72-78.] | |

| [26] | Zhu ZX, Zhang LR, Liu Y, Meng R, Jin SC (2025) Business biodiversity conservation: International progress and enlightenment. Acta Ecologica Sinica, 45, 6131-6141.(in Chinese with English abstract) |

| [朱振肖, 张丽荣, 刘洋, 孟锐, 金世超 (2025) 工商业生物多样性保护: 国际进展与启示. 生态学报, 45, 6131-6141.] |

| [1] | 张晋越, 卞宝乐, 唐泰然, 农文豪, 朱书峰, 卢新民. 植物-根际微生物互作及对昆虫胁迫的响应[J]. 生物多样性, 2026, 34(4): 25334-. |

| [2] | 蒋翠憶, 谢致敬, 田中平, 李玥莹, 郑明心, 房帅, 米尔卡米力∙麦麦提, 依里帆∙艾克拜尔江, 高梅香, 张健. 微地形生境异质性对新疆西天山森林土壤跳虫群落分异的塑造作用[J]. 生物多样性, 2026, 34(4): 25300-. |

| [3] | 张霜, 宋波. Meta分析应用中应注意的几个关键问题[J]. 生物多样性, 2026, 34(1): 25308-. |

| [4] | 刘志祥, 谢华, 张慧, 黄晓磊. 表皮碳氢化合物在社会性昆虫中的功能多样性及其调控[J]. 生物多样性, 2025, 33(2): 24302-. |

| [5] | 陈瑶琪, 郭晶晶, 蔡国俊, 葛依立, 廖宇, 董正, 符辉. 近七十年(1954-2021)长江中下游湖泊沉水植物群落多样性演变特征[J]. 生物多样性, 2024, 32(3): 23319-. |

| [6] | 杨舒涵, 王贺, 陈磊, 廖蓥飞, 严光, 伍一宁, 邹红菲. 松嫩平原异质生境对土壤线虫群落特征的影响[J]. 生物多样性, 2024, 32(1): 23295-. |

| [7] | 王明慧, 陈昭铨, 李帅锋, 黄小波, 郎学东, 胡子涵, 尚瑞广, 刘万德. 云南普洱季风常绿阔叶林不同种子扩散方式的优势种空间点格局分析[J]. 生物多样性, 2023, 31(9): 23147-. |

| [8] | 谢艳秋, 黄晖, 王春晓, 何雅琴, 江怡萱, 刘子琳, 邓传远, 郑郁善. 福建海岛滨海特有植物种-面积关系及物种丰富度决定因素[J]. 生物多样性, 2023, 31(5): 22345-. |

| [9] | 李艳辉, 兰天元, 王月, 于洋, 赵常明, 李利华, 徐文婷, 申国珍. 神农架植物物种空间周转的驱动因素[J]. 生物多样性, 2022, 30(4): 21377-. |

| [10] | 韩雪, 苏锦权, 姚娜娜, 陈宝明. 外来入侵植物的根系觅养行为研究进展[J]. 生物多样性, 2020, 28(6): 727-733. |

| [11] | 孙远, 胡维刚, 姚树冉, 孙颖, 邓建明. 黄河流域被子植物和陆栖脊椎动物丰富度格局及其影响因子[J]. 生物多样性, 2020, 28(12): 1523-1532. |

| [12] | 周昌艳, 王彬, 邓云, 乌俊杰, 曹敏, 林露湘. 林冠结构是局域尺度木本植物功能性状beta多样性形成的重要驱动力[J]. 生物多样性, 2020, 28(12): 1546-1557. |

| [13] | 杨贵军, 王敏, 杨益春, 李欣芸, 王新谱. 贺兰山甲虫物种丰富度分布格局及其环境解释[J]. 生物多样性, 2019, 27(12): 1309-1319. |

| [14] | 刘硕然, 杨道德, 李先福, 谭路, 孙军, 和晓阳, 杨文书, 任国鹏, Davide Fornacca, 蔡庆华, 肖文. 滇西北高山微水体与溪流生境底栖动物多样性和环境特征[J]. 生物多样性, 2019, 27(12): 1298-1308. |

| [15] | 张宇, 冯刚. 内蒙古昆虫物种多样性分布格局及其机制[J]. 生物多样性, 2018, 26(7): 701-706. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

备案号:京ICP备16067583号-7

Copyright © 2026 版权所有 《生物多样性》编辑部

地址: 北京香山南辛村20号, 邮编:100093

电话: 010-62836137, 62836665 E-mail: biodiversity@ibcas.ac.cn

![]()